Robert Speed

Principal

A question is often asked of us about the different ways to structure a company’s share capital. Below is a summary of the Australian legal position and practice with respect to the share capital of an Australian company. It focuses on private companies (ie. companies not listed on ASX).

Section 114 of the Corporations Act states that a company must have at least one member. Membership in a company limited by shares (as opposed to a company limited by guarantee) is conveyed upon the holder of a share or shares. That means that a company limited by shares must have at least one shareholder.

While a share may be tangible, in the sense that it may be represented by a physical or electronic certificate, it is also appropriate to view a share as a thing to which a bundle of intangible rights and restrictions of the shareholder are “attached” in respect of the company and its other shareholders.

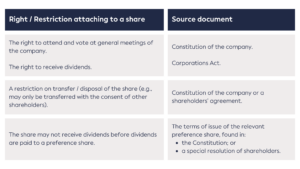

A company is broadly empowered by section 254B of the Corporations Act to determine the terms on which shares are issued and the rights and restrictions attaching to them. These can be set out in a range of sources, including:

each of which can determine how the shares in the company operate with respect to the company and each other.

An example is set out in the table below.

Companies have a great deal of flexibility when it comes to how they structure and issue share capital. This is reflected in the Corporations Act, which sets no limits with respect to the share structure of a company (other than section 254A(3) of the Corporations Act, which stipulates that redeemable shares are preference shares, discussed further below).

Usually, a company’s main class of shares is referred to as ‘ordinary shares’. The Corporations Act does not provide a definition for an ordinary share. Ordinary shares are generally considered the least burdensome form of capital instrument that may be issued by a company (and conversely highest risk form of instrument to a holder) – as they do not have any right to repayment or redemption by the company, nor any right to specified dividends or distributions. On a liquidation they rank last in terms of a return of capital to holders of capital instruments, but on the other hand may participate in any surplus remaining once preferred forms of capital instruments have been repaid.

Typically, the constitution of a company will provide ordinary shareholders with the right to:

Either the constitution or a shareholder’s agreement may also provide for:

The Replaceable Rules set out in the Corporations Act, if applicable to a company, operate to grant similar rights to shareholders, however those rules do not specifically apply to ‘ordinary’ shares, but just shares.

On the question of whether a company needs to issue ordinary shares before issuing any other form of share, the High Court of Australia in Beck v Weinstock (2013) 251 CLR 425:

The second point arose because the dispute in the case occurred in circumstances where:

Beck argued that because the company only purported to have preference shares on issue, the redeemable preference shares did not have a real preferential right (as there was no existing ordinary shares over which they were preferred), could not be genuine preference shares and therefore their redemption could not occur by reason of section 254A(3) of the Corporations Act (this section requires that only preference shares may be issued on terms that they are redeemable).

The High Court found for Weinstock and ruled that, provided a preference share was issued on terms which gave it a preferential right over ordinary shares, it was still a preference share despite no ordinary shares ever being issued.

This suggests that a company need not have ordinary share capital on issue, despite some of the possible unusual situations that could arise, such as no shareholder being able to vote in a general meeting of the company (since preference shares are usually non-voting).

The High Court suggested these absurdities could, and would, be avoided by a board ensuring that if necessary ordinary shares be issued, so that a general meeting could proceed. However, a company cannot compel someone to subscribe for ordinary shares, so it may not be in the directors’ control to ensure this occurs.

Despite this High Court authority, we do not recommend companies follow this approach of not having any ordinary share capital on issue.

Unlike other forms of shares, the Corporations Act and the courts have set some requirements for rights attaching to a class of shares if they are to be considered preference shares, being:

Provided that the above mentioned requirements are satisfied, the kinds of rights (and restrictions) which can be attached to preference shares are theoretically limitless but tend to fall into several common categories:

The way in which preference shares often have a right to a fixed dividend and/or a return of capital upon liquidation mirrors the rights commonly attributed to types of debt, and in fact preference shares are regarded as a type of “hybrid” financial instrument, in that they have characteristics of both, and are therefore a hybrid of, debt and equity.

Liquidation Preference Shares are commonly used by private equity investors to limit downside risk and increase the certainty of their expected returns. Liquidation Preference Shares may also:

Preference shares may also be:

In considering the issue of preference shares, it is important to ensure that their rights are clearly documented, not only to ensure compliance with section 254A of the Corporations Act, but because:

Still relatively uncommon in the Australian corporate environment, these shares are used more often in the United States and may:

Founder shares may also be “deferred” which means that they only entitle their holders to receive a dividend after a specified minimum has been paid to ordinary shareholders.

Within the private context it is difficult to say with certainty why founder shares have not been more widely adopted in Australia, however voting power will often be managed with the distribution of voting (i.e., ordinary) shares and non-voting classes of shares. In the listed environment the position is clearer cut, with the ASX taking a negative view on the inclusion of any “super” voting shares in the capital structure of a listed entity.

In establishing a share capital structure, companies should also be aware of the provisions in the Corporations Act which apply to:

Under section 246B of the Corporations Act:

Under section 246C of the Corporations Act:

Under section 246D of the Corporations Act, unless all holders of shares in a class consent to the variation or cancellation of their rights, shareholders holding at least 10% of the votes in the class may apply to the court to have the variation set aside. This also applies where the constitution is varied to permit a variation or cancellation of rights attaching to shares in a class if the resolution to vary the constitution is not unanimous.

A multi-class share structure, whether implemented intentionally or unintentionally, can have implications for the company as it may impact the governance and administration requirements of the company by:

Given the risk of inadvertently creating a new class of shares or performing an action amounting to a variation of class rights, we recommend that any company looking to issue shares or altering the rights attaching to shares first seek legal advice.

If considering implementing or changing a corporate structure by way of the issue of shares, directors should remember that:

On 14 November 2024, the Treasury released an exposure draft of the Treasury Laws Amendment Bill 2024: Enhanced Disclosure of Ownership of Listed Entities (Draft Bill) and opened consultation in relation to the Draft Bill.

This article discusses the requirements of a valid share transfer in accordance with the Corporations Act 2001 (Cth) and the adverse consequences that may arise from an invalid transfer.